Master Your Retirement: How to Calculate Annuity Rate of Return

Planning for a secure retirement requires choosing financial options that promise stability, predictable growth, and a lifetime income stream. Among the various wealth accumulation tools available, annuities are widely popular for their ability to convert upfront savings into guaranteed payouts. However, to truly understand if these financial options are serving your long-term goals, you must know how to evaluate their efficiency. Learning how to estimate investment returns via an accurate calculation prevents you from overpaying for fees or locking your capital into low-yielding contracts. In this ultimate guide, we will break down the mathematical formulas, performance metrics, and strategic steps needed to evaluate your options and secure your financial future.

What Is Return on Investment (ROI) and How to Calculate It

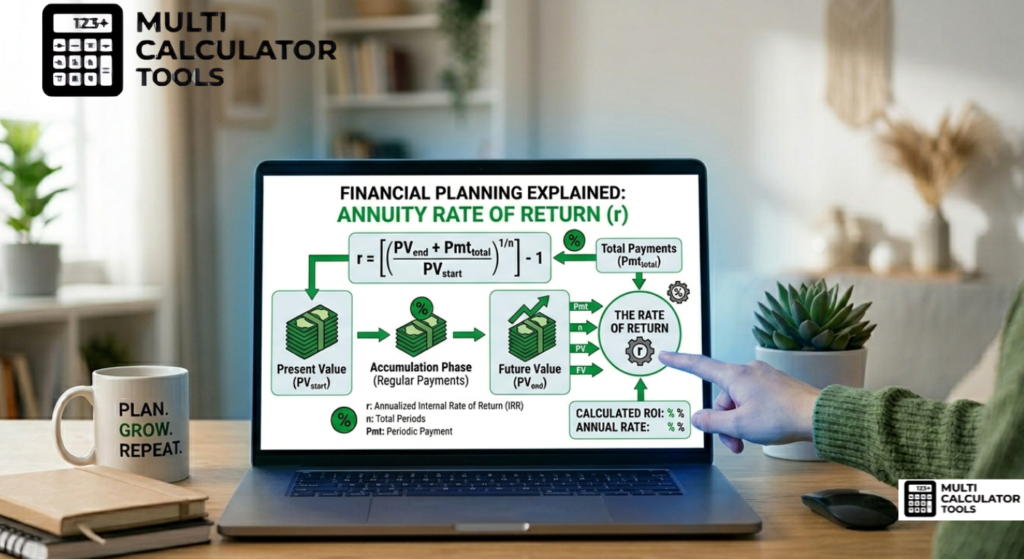

Evaluating a new financial choice without a clear math metric is like building a house without a blueprint. To successfully build wealth and make data-driven decisions, individuals and corporations rely on a standardized process to evaluate performance metrics. The annuity rate of return formula is used to measure the overall profitability of an annuity investment by evaluating how much income it generates over time. Whether using an annuity return calculator, calculating the rate of return on annuity, or performing a full annuity return calculation, investors aim to understand the effectiveness of their long-term savings. The process of calculate annuity rate of return involves analyzing contributions, interest rates, and time periods to determine total earnings. This foundational step removes the guesswork from your retirement strategy.

Key Takeaways

The core definition of this metric revolves around measuring the overall efficiency and profitability of a specific financial commitment over time. The inherent versatility of the math means it applies universally across completely different options, ranging from immediate income payouts to deferred tax-advantaged growth plans. However, context remains highly critical, which means a standalone percentage is practically meaningless unless you factor in the length of time the money was held, ongoing contract maintenance fees, and original capital costs.

What Is Return on Investment (ROI)?

Return on Investment is a fundamental financial ratio used to evaluate the profitability of a resource layout relative to its initial cost. When you attempt to evaluate a corporate project or an equity purchase, you are looking for a clear percentage that reveals how hard your money is working for you. An annuity investment return formula helps estimate expected payouts, while an annuity ROI calculator simplifies the process of evaluating performance. Tools such as an annuity earnings formula or annuity growth calculator are commonly used in retirement annuity return calculation to project future income streams. A fixed annuity rate of return provides stable and predictable earnings, whereas a variable annuity return formula reflects market fluctuations and changing investment conditions. It transforms complex insurance contract ledger items into a single, highly readable number that anyone can easily understand.

How to Calculate Return on Investment (ROI)

To accurately evaluate performance, you must understand the math that calculates the movement of money across different periods. This math relies entirely on compound interest, which means you earn interest on your initial principal plus all the previous interest you have accumulated over the years.

The universal mathematical formula for compound interest future value is represented as:

$$FV = P\left(1+\frac{r}{n}\right)^{nt}$$

Inside this equation, $FV$ represents the future value of the money, $P$ stands for the initial principal amount, $r$ is the annual nominal interest rate, $n$ is the compounding frequency per year, and $t$ is the total number of years the money compounds. Overall, an annuity performance calculator and annuity investment analysis help investors compare options, assess risk, and estimate future returns. Accurate annuity return estimation supports better financial planning, wealth accumulation, and long-term retirement security.

Why Is ROI a Useful Measurement?

The widespread popularity of this metric stems from its absolute simplicity and universal application. It serves as a standardized financial benchmark that allows investors to rank completely different investment structures against one another. Understanding annuities begins with the present value of annuity and future value of annuity, which are key concepts in evaluating how money grows over time through compound interest. These calculations often include periodic payments and an interest rate calculation to determine the total value of an investment or payout stream. In retirement income planning, annuities play a major role in ensuring stable investment growth and predictable annuity payments over time. If a person needs to choose between buying a rental property or securing an insurance contract, a quick calculation provides a direct, head-to-head comparison to maximize wealth efficiency.

What Are the Limitations of ROI?

While incredibly helpful, relying blindly on a basic calculation can lead to dangerous financial oversight. The primary limitation is that a standard raw formula does not automatically account for the subtle penalties associated with early cash withdrawals or structural contract riders. For instance, a high paper return looks amazing, but it is vastly different if high insurance fees absorb a massive portion of those gains over a ten-year horizon. Additionally, standard equations fail to account for market volatility or the emotional stress involved when a variable contract declines during a sharp economic downturn. Through financial forecasting and the principles of time value of money, investors can better estimate investment returns and understand the annual return percentage they may receive.

What Is a Good ROI?

In the United States financial markets, a conventional rule of thumb dictates that a conventional return above seven percent to ten percent is considered good for aggressive equity investments, as this aligns with the historical average of the stock market. However, a “good” return is highly dependent on your specific age, timeline, and your personal tolerance for financial risk. Annuities are widely used for wealth accumulation and retirement savings, supported by detailed cash flow analysis to track income and expenses. Whether dealing with a fixed annuity or a variable annuity, understanding investment performance is essential for effective long-term financial planning and accurate earnings projection. A safer contract will naturally yield a lower, more predictable percentage than a high-risk growth portfolio.

Case Study: Applied Value Investing

For professionals and advanced students aiming to master economic moats and corporate valuations, structured educational pathways provide immense value. Premium programs such as the Wharton Online and Wall Street Prep Applied Value Investing Certificate offer rigorous, hands-on training frameworks. These programs bridge the deep gap between complex academic accounting theories and real-world wealth management practices, helping individuals make better financial decisions regarding complex lifetime cash flows.

What Are the Wider Applications of ROI?

Beyond traditional stock market portfolios, the math used to evaluate performance plays a massive role in modern retirement infrastructure. These tools contribute to greater financial security, improved capital growth, and more reliable income stream analysis during retirement. The table below highlights how different financial products perform across various planning parameters:

| Product Type | Primary Growth Engine | Predictability Level |

| Fixed Contract | Guaranteed Interest Rate | High Certainty |

| Variable Contract | Mutual Fund Sub-accounts | Market Dependent |

| Index-Linked Plan | Market Index Performance | Moderate Caps |

Explain It Like I’m Five

Imagine you have a magical piggy bank where you drop ten dollars every single month. Instead of just holding your cash, the piggy bank adds extra coins inside as a reward for leaving your money alone. At the end of the year, you discover you have more money than you originally put in. Calculating your rate of return is simply a way to show exactly how many extra coins that magical piggy bank gave you for your patience.

Fast Fact

Key financial inputs such as the discount rate are crucial in shaping retirement investment strategy and ensuring balanced portfolio diversification. Statistics show that individuals who use automated tracking tools to run regular calculations achieve fifteen percent higher clarity regarding their final nesting egg targets than those who guess.

What Is ROI in Simple Terms?

In simple terms, ROI is the financial scorecard of your hard-earned money. It tells you exactly whether a financial choice was a smart option that made you richer, a break-even choice that kept you stagnant, or an inefficient choice that shrank your spending power due to inflation. It takes away the complicated industry jargon and replaces it with a simple percentage that guides your next step.

Is ROI Calculated Annually?

By default, a standard baseline calculation does not automatically adjust for an annual timeframe. Because of this, experienced financial analysts prefer to use an annualized formula. This advanced calculation normalizes the holding period of an asset, allowing you to see your geometric average growth rate per year so you can compare long-term and short-term choices fairly. It prevents a thirty-year contract from looking artificially better than a high-yielding short-term bond.

How Do You Calculate Return on Investment (ROI)?

To execute a flawless calculation inside a personal spreadsheet layout, you must map out your cash inflows and outflows cleanly.

| Financial Variable | Spreadsheet Mapping | Data Input Example |

| Initial Capital Outlay | Input Field One | $50,000 |

| Final Accumulated Value | Input Field Two | $75,000 |

| Automated Math Formula | Calculation Row | = (Value – Cost) / Cost |

| Calculated Percentage | Output Display | 50% |

What Industries Have the Highest ROI?

Historically, industries with low physical overhead and high scalability yield the highest immediate return metrics. Software and technology companies lead the global market because low replication costs allow for exponential profit margins once the initial platform is built. Pharmaceuticals also rank incredibly high, where massive initial research costs are offset by high margins once a patent is secured. Real estate remains a favorite for using borrowed bank money to amplify returns, while insurance-backed contracts excel at protecting that wealth once it has been generated.

The Bottom Line

Learning how to calculate your true performance metrics is the ultimate cornerstone of sound retirement decision-making. Advanced financial modeling helps individuals evaluate savings growth, manage risk and return assessment, and optimize lifetime income planning for sustainable financial stability throughout retirement. By stripping away emotional biases and focusing strictly on hard percentages, you can eliminate hidden fees, optimize your asset distribution, and ensure your money compounds safely over time.

Related Articles

- How to Build a Lifetime Income Spreadsheet in Excel

- Understanding the Difference Between Fixed and Variable Options

- The Impact of Modern Inflation on Long-Term Payout Streams